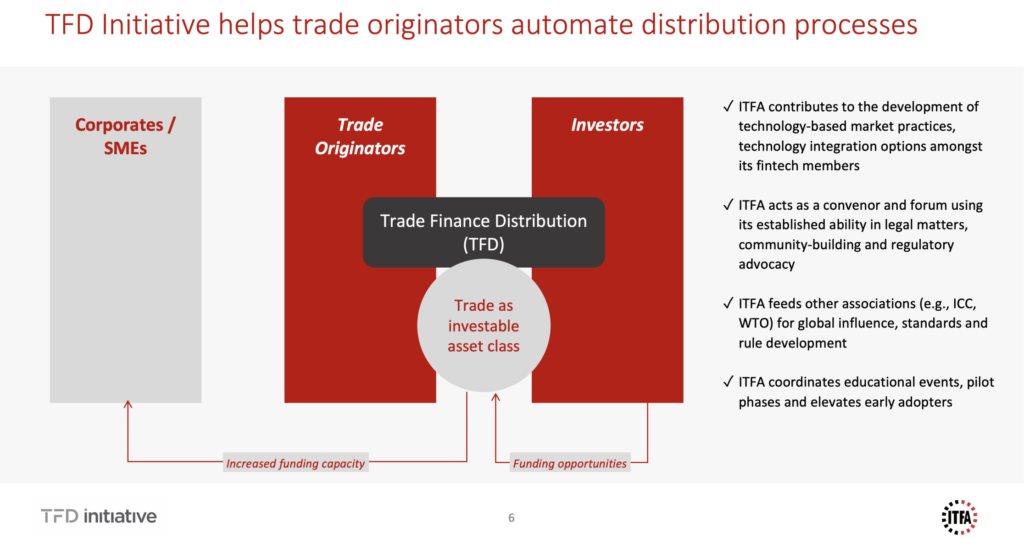

ITFA represents the rights and interests of banks, financial institutions and service providers involved in trade risk and asset origination and distribution.

Our Mission

ITFA > Newsletters > MAKING TRADE INVESTIBLE FOR INSTITUTIONAL INVESTORS – BANKS MAKE IT HAPPEN, Dec 2020

MAKING TRADE INVESTIBLE FOR INSTITUTIONAL INVESTORS – BANKS MAKE IT HAPPEN, Dec 2020

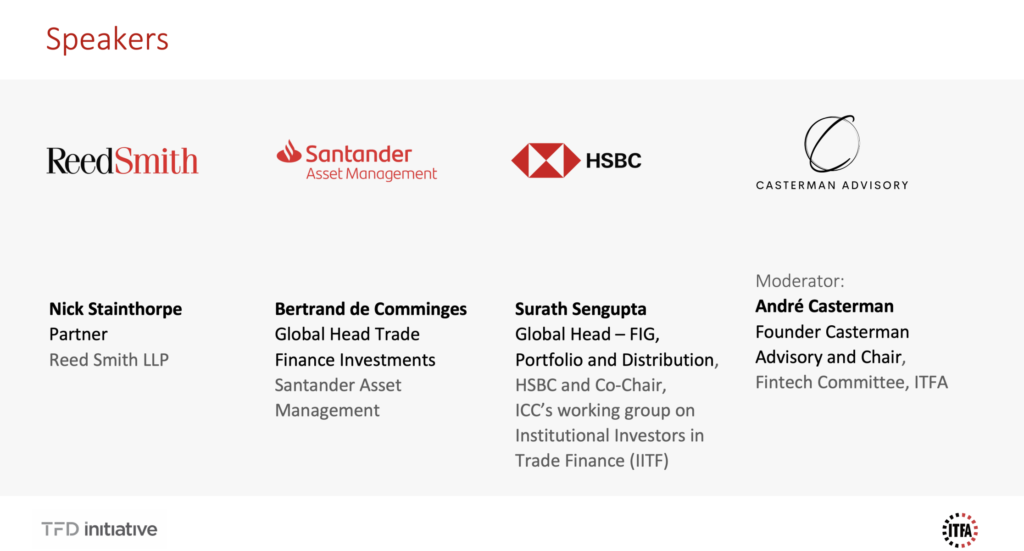

By André Casterman, Founder and Managing Director, Casterman Advisory and Chair of Fintech Committee, ITFA

Collaboration,

Innovation, Standardisation and Education were the keywords that our panellists

representing HSBC, Reed Smith and Santander Asset Management highlighted during

our recent TFD Initiative webinar. The session demonstrated how making trade

investible for institutional investors is being achieved by top players in the

industry, and how new long-term partnerships will help fill the trade finance

gap.

The

Wall Street Journal of 22 January 2020 featured an article entitled “Money managers, Lured by Rich Returns, Venture Into Risky World of Trade

Finance“: “… large money managers buy trade-finance

assets that lenders have already originated instead of funding importers and

exporters directly. Often these assets are wrapped up into asset-backed

securities.”. In this article, Surath Sengupta, global head of

FIG, Portfolio and Distribution at HSBC, said “HSBC has

increased the trade financing it sells on to investors and other lenders from

$2 billion in 2015 to $28 billion last year [2019].”

This

illustrates a key trend as originating banks are expanding their distribution

network to new types of funders in order to grow their own trade financing

capacity. Rather than limiting themselves to the niche inter-bank space, more

banks start partnering with a range of institutional investors and are

therefore making trade assets more accessible to those non-bank funders through

securities formats such as asset-back notes.

This

is a strategic theme for the ITFA membership which is why I invited the

following early adopters of TFD Initiative:

We

collected the following take-aways and questions from the audience.

Take-aways on working

with institutional investors

Trade finance is attracting new funders that recognise

the key attributes of this asset class; particularly the absence of

correlation with other investment classes. The ESG priority on the asset

management side is also triggering higher interest for trade finance given

the sustainability-related transparency that trade flows offer.

In order to make trade finance more accessible to

institutional investors, we need to build the bridge between the two

spaces: trade finance and capital markets. This way, trade finance assets

will become accessible outside the traditional inter-bank and credit

insurance spaces.

Trade finance is traditionally supported by banks’ own

balance sheets. The Master Participation Agreement (MPA) is well suited

for expert investors such as banks’ trade finance teams. However, in some

cases, institutional funders can only invest in securities (e.g., notes)

as required by their mandate. This is why trade assets need to be

repackaged into such notes via a Special Purpose Vehicle (SPV).

Asset-backed notes are widely used in the capital

markets across a multitude of investment classes. For example, the use of

notes would facilitate the role of asset managers and other institutional

liquidity providers investing in trade assets originated by top banks.

Some enhancements can be added via the SPV to improve

the investment profile of the underlying trade finance assets e.g.,

insurance held by the SPV, risk reserves and pooling of diversified

assets. In trade finance, we often refer to “repackaging” rather

than “securitisation” to pass on the corporate risk and reward

of the underlying assets to the investor. These SPVs could be independent

entities that banks use or may be offered by third-party service providers

such as the Trade Asset Securitisation Company (TASC).

Take-aways on types of trade asset transfers

There are two ways to transfer of assets: (1) funded

transfer corresponding to the sale of the asset and (2) unfunded transfer

of the risk. The potential is enormous on single transactions or on

portfolios of transactions. Both can be supported by a SPVs and securities

format (e.g., notes).

Some institutional investors have developed the

appropriate internal trade finance expertise and are happy to participate

in transactions via the MPA, but many capital market institutions favour

investing through securities – as they do with other asset classes – which

is why “repackaging” is the strategic option for banks wishing

to engage with those funders. There can be challenges on the regulatory

and tax sides but these obstacles are navigable.

By using “notes”, it’s possible to grow

institutional funding but we need scale volumes under the structures in

the short term to defray costs. Banks can also use notes when investing in

trade assets, not only institutional investors. In case of default of the

underlying assets, the notes structure protects the investors through the

physical settlement option: the investors can redeem their notes in return

for receiving the assets directly.

Santander Asset Management runs a Trade Finance fund

where the institutional liquidity is pooled. The notes produced by TASC

are purchased by the fund. The SPV – TASC in this case – signs MPAs with

each originating bank and following Santander Asset Management fund

manager’s guidance. The whole model is scalable and secure for all parties

as the ultimate goal is to bring a stable source of liquidity and high

quality investments to, respectively, participating originators and

investors.

Trade Finance historically benefits of lower rates of

default than other asset classes. Saying that, fraud risk is a risk that

is very difficult to spot for this or any other asset class. Banks may

need to find ways to decouple the fraud risk from the credit risk in some

situations for institutional investors. There are many ways for banks to

mitigate fraud risk thanks to the various touch points and relationships

that banks entertain with those corporates. As volumes grow, the

diversified nature of many receivables and payables portfolios also help

dilute the adverse effects of fraudulent transactions for institutional

investors.

Take-aways on the benefits for corporates, banks and

funders

Large corporates and regional companies expect stable and reliable sources of liquidity

from their banking partners. By relying on a range of institutional

investors, originating banks increase their capacity and can serve their

clients better and in a more consistent way. In this new model, banks act

as intermediators relying on new sources of liquidity.

For originators such as HSBC, sharing trade assets

with institutional funders provides a path to grow revenues, support clients and develop trade as an asset

class whilst lowering capital requirements, this making

the bank is benefiting strongly from such

“originate-and-distribute” model by (1) continuously redeploying

the capital being freed up thanks to distribution to institutional

investors (2) strengthening relationships with its top clients thanks to

higher diversified liquidity (3) arranging the right level of liquidity in

specific currencies. The impact on return on equity for banks is very

positive which is why such activity as become strategic for banks.

The risk that institutional investors would leave the

trade asset class when macro-economical conditions change is low. Once the

investors understand the value, the risk profile and yields of trade

finance, they remain committed to the investment opportunity that trade

offers. The growing importance of ESG will further increase the attractiveness

of the asset class.

Santander Asset Management Trade Finance fund, which

is EUR denominated, is attracting multiple type of investors: (1)

traditional CP and/or money market investors such as pension funds and

insurance companies looking for long-term participations into the fund (2)

larger corporate players with significant liquidity looking for more

tactical solutions; and, (3) high leverage first-loss investors looking

for higher returns. There is a clear market interest in this asset class as

presented by Santander Asset Management. They key attributes of trade

finance, paired with the right asset class knowledge and expertise of the

Fund managers, make these assets more and more understood by the investors

as outlined below:

“For

originators such as HSBC, sharing trade assets with institutional funders

provides a path to grow revenues, support clients and develop trade as an asset

class whilst lowering capital requirements”, Surath

Sengupta, Global Head – FIG, Portfolio and Distribution,

HSBC and Co-Chair, ICC’s working group on Institutional Investors in Trade

Finance (IITF)

“Large

corporates and regional companies expect stable and reliable sources of

liquidity from their banking partners. By relying on a range of institutional

investors, originating banks increase their capacity and can serve their

clients better and in a more consistent way”, Bertrand

de Comminges, Global Head Trade Finance Investments, Santander Asset Management

Questions from audience

How expensive is it to have a trade asset

securitisation put in place by an institution? Is the cost depending on size of

the portfolio? Or other fixed charges to take into account?

Please

contact us for pricing details. The TASC option offers repackaging-as-a-service

which is a way to share most of the set-up costs.

Is there a legal mismatching

with the instruments underlying governing law, i.e., L/C issued in Bangladesh

or Nigeria, and the law governing the SPV?

Please

contact Nick Stainthorpe.

Regarding short-term trade

finance how can you insure a stable pool of liquidity and preserve client

relationships as investors may use such funds as liquidity parking?

Please

contact Bertrand de Comminges.

While clients are trusted

counter-parties, under stress some clients could commit fraud. As an investor,

I would like to know whether you protect yourselves in any way against the

fraud risk? Or do you rely solely on the relationship of the lender – borrower?

Please

see above key take-aways on fraud risk.

I am interested to hear

panellists’ views on 1) large corporate clients’ whose trade assets are being

repackaged into securities cannibalising and contaminating their existing bond

yield curve and 2) MNPI issues now that we have a security format and the

complicated issues around that.

Please

contact Christoph Gugelmann, CEO, Tradeteq.

Investors also participate

directly under MRPAs – I wonder if in general Trade Finance, being a

relationship driven business, is not often too finely priced to pay for setting

up SPVs with all the legal costs related to this.

The

Trade Asset Securitisation Company (TASC) offers a way to share those costs.

Do banks make a market in the

secondary space for these notes if necessary? i.e., if the investor wants to

sell before maturity would the bank buy it back? There would clearly be an

illiquidity discount but trying to understand if at all possible. This would be

key especially for funds offering daily liquidity.

Please

contact Christoph Gugelmann, CEO, Tradeteq.

ITFA represents the rights and interests of banks, financial institutions and service providers involved in trade risk and asset origination and distribution.Our Mission

ITFA represents the rights and interests of banks, financial institutions and service providers involved in trade risk and asset origination and distribution.Our Mission